Hormuz Crisis Could Trigger New Wave of LNG Project FIDs

A new Wood Mackenzie analysis shows how the Strait of Hormuz crisis could reshape global LNG markets, influence project sanctions and alter long-term supply and demand trends.

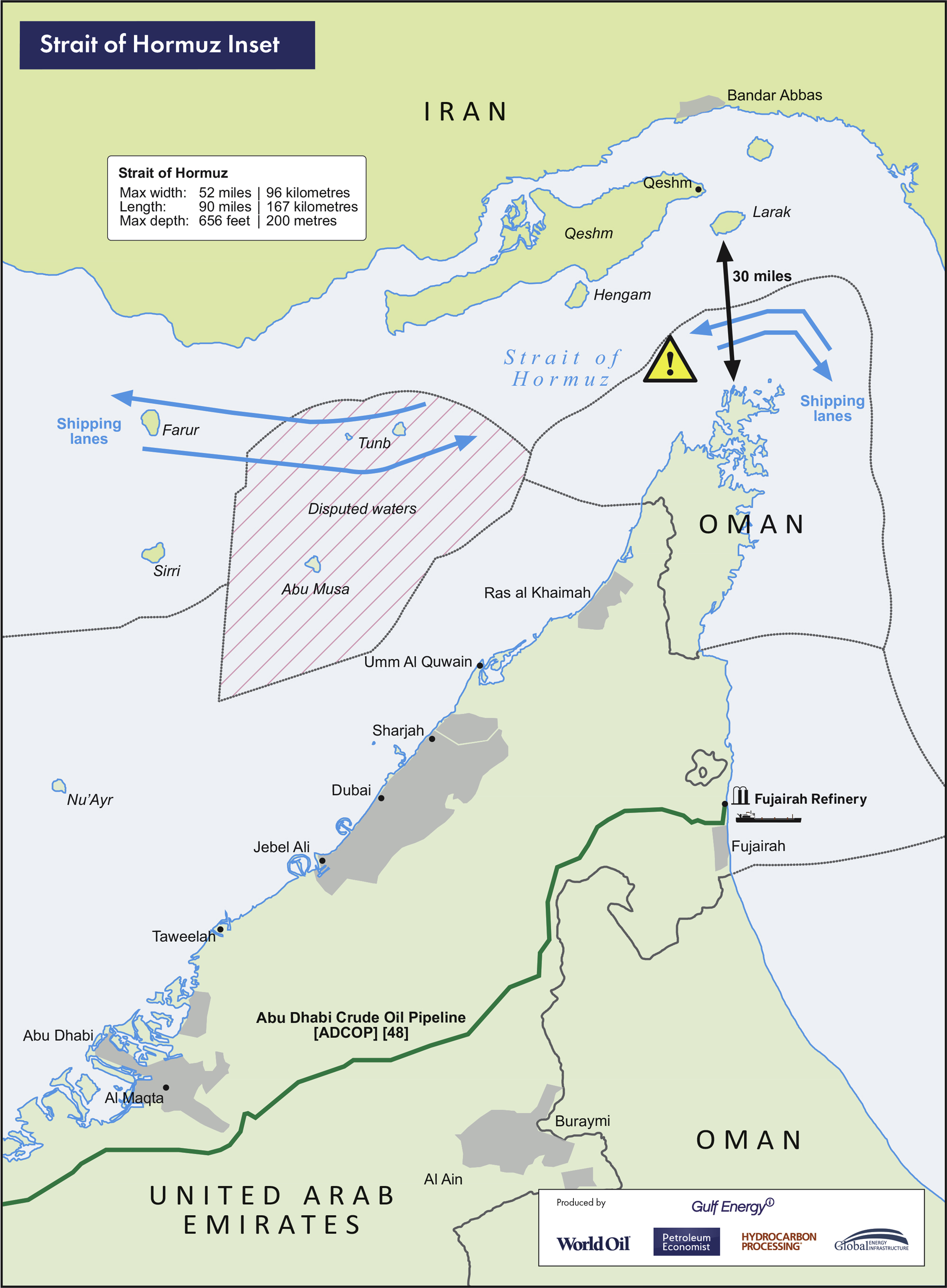

(P&GJ) — Global LNG markets could face years of uncertainty following the closure of the Strait of Hormuz, with new LNG export projects outside the Middle East potentially benefiting from a prolonged disruption, according to a new analysis from Wood Mackenzie.

The consulting firm modeled three potential market outcomes based on how quickly the conflict is resolved and how soon the Strait of Hormuz reopens. The disruption has removed more than 80 million metric tons per annum (MMtpy) of LNG supply from global markets, equal to roughly 20% of worldwide LNG production.

Under its most optimistic scenario, Gulf LNG facilities resume operations this year and return to full capacity by 2027. A more prolonged disruption could delay production recovery until 2028, while the firm's most severe scenario assumes recurring conflict and infrastructure damage that permanently reduces expected Middle East LNG growth. In that case, major projects could face years of delays and some planned developments may never reach FID.

Wood Mackenzie said LNG supply growth outside the Persian Gulf remains robust, with more than 150 MMtpy of export capacity already under construction, largely in the United States. The firm also expects more than 30 MMtpy of additional LNG projects to reach final investment decision by the end of 2027. A prolonged supply disruption could encourage developers to accelerate project sanctions outside the Middle East.

"The Strait of Hormuz closure has done more than remove LNG from the market. It has removed certainty," Kateryna Filippenko, research director for global gas markets at Wood Mackenzie, said in a statement. She added that the key challenge for buyers, investors and policymakers is whether supply portfolios are resilient enough to withstand a range of market outcomes.

The report also found LNG demand is expected to grow under all three scenarios, although some importing nations may seek to reduce dependence on LNG over time through fuel diversification strategies. Market balances and prices vary significantly across the scenarios, with the most severe disruption producing prolonged volatility and tighter supply conditions through the end of the decade.